- Total revenue: price x quantity

- You can find it on the demand and supply graph. The area until equilibrium.

- Average revenue: total revenue/ quantity = price

- Marginal revenue: additional revenue from the next item sold

- When demand is price inelastic, you can raise prices and total revenue will not decrease.

- When demand is price elastic, firms can raise prices but total revenue will fall.

- Total cost: total fixed cost +total variable cost

- Total fixed cost: costs that do not vary with output e.g. rent

- Total variable cost: costs that do vary with output e.g. ingredients

- Average (total) cost: total cost divided by output

- Average fixed cost: fixed cost divided by output

- Average variable cost: variable cost divided by output

- Marginal cost: the extra cost of producing one extra unit.

- Diminishing marginal productivity: when you hire more workers, each worker slows down because they are sharing the same fixed factors e.g. 5 chefs in the same kitchen.

- Short-run: when there is at least one fixed factor of production.

- Long-run: when all factors are variable.

- Average cost curve: U-shaped

- Marginal cost curve: tick shaped

- Average revenue: downward sloping (demand curve)

- Marginal revenue: twice as steep as the AR curve.

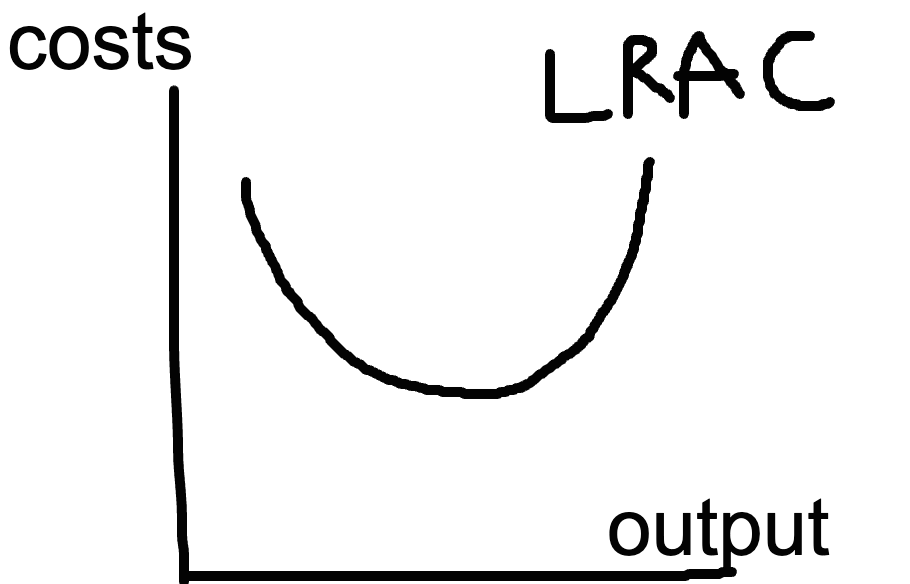

- Economies of scale: when long-run average costs fall as output increases.

- Really Fun Mums Try Making Pies

- Risk (new recipe)

- Financial (access to finance)

- Marketing (every little helps)

- Technical (self checkouts)

- Managerial (easier to delegate work)

- Purchasing (bulk-buying)

- Diseconomies of scale: when long run average costs rise as output increases.

- coordination (difficult to manage the staff)

- control (difficult to identify weak spot)

- communication (workers feel alienated)

- Minimum efficient scale: the minimum level when a firm can first start to exploit maximum economies of scale.

- Internal economies of scale: affect one firm.

- External economies of scale: affect the entire industry.

- transport

- education and training

- infrastructure

- Profit maximisation: MC = MR

- Short-run shutdown points: when AC>AR